Galaxies (Operating Systems) Collide with Planets (Apps)

Galaxies (Operating Systems) Collide with Planets (Apps)

Operating systems and software applications fight over where does the customer relationship live

Twitter:@arthurtyson3

Over the past few weeks, we have witnessed software applications (planets) collide with operating systems (galaxies), causing some software apps to be removed from the operating systems’ platforms. Peacock and HBO Max were unable to complete Smart TV distribution deals with Amazon and Roku, and Fortnite was removed from Apple’s iOS platform for enabling payments within its application. At the crux of this tension between services is “where does the customer relationship live?” The operating systems would like to continue to own the customer relationship to ensure that software services orbit within their galaxy, and software services aspire to own the customer relationship so that they can evolve from planets into their own galaxies—the operating system of a specific human need. We see this astronomical collision take place in the universes of Smart TVs and smartphones.

Smart TVs: Customer Relationship Orbits Here Not There

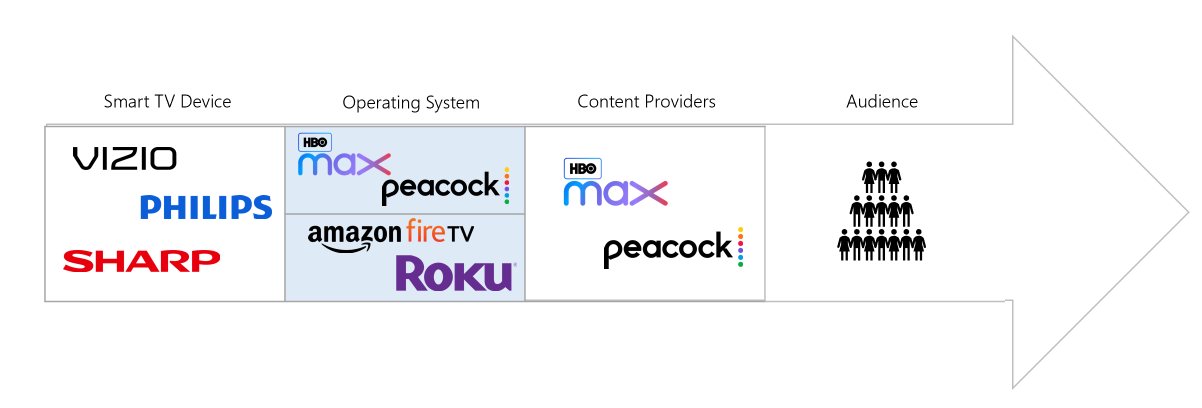

During the pandemic, the Smart TV universe rapidly expanded as video streaming increased by 63%. The primary beneficiaries of the increased usage were the galaxies—Smart TV operating systems: Roku and Amazon Fire, which own 65% share of total Smart TV viewing hours. Noticing this fortuitous moment for media consumption, Warner Media and NBC Universal right-sized their operations from physical distribution to digital to release their own D2C video streaming offering, HBO Max and Peacock. After securing distribution in other universes: smartphone, tablet, and game consoles, the final universe to secure distribution — where the most “lean back” TV viewing happens— is Smart TVs.

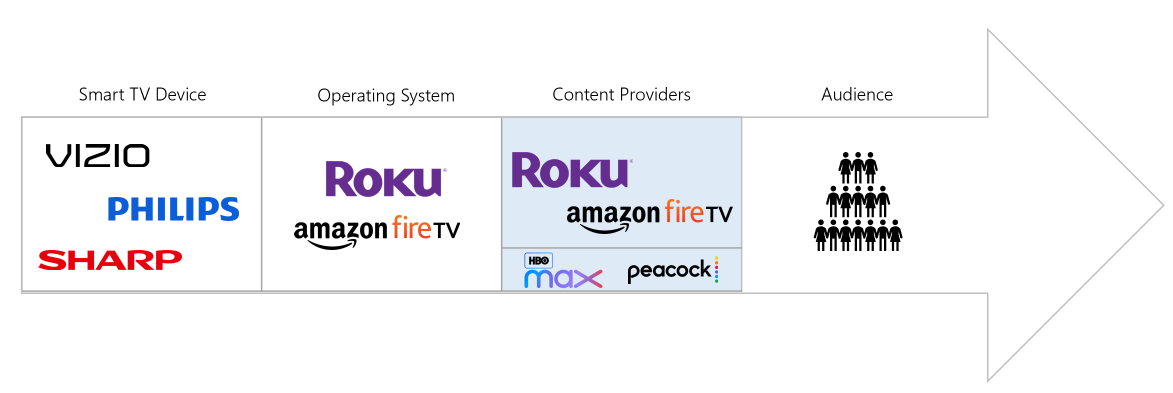

HBO Max and Peacock broached the two largest galaxies (Roku and Amazon) in the Smart TV universe about negotiating a distribution deal. Each side was able to quickly come to an agreement on revenue share—a platform (galaxy) fee per subscriber (Amazon: 15%-45% and Roku: 20%)—but where the friction lied in the negotiations is where the video experience will reside. The operating system providers have mandated that the video experience resides on their channels to ensure that these services orbit within their galaxy, but the content providers want users to be pushed from the OS to their video streaming applications (planets). This nuance of where video streaming takes place matters because, “he who owns the video experience, controls the customer relationship (the data).” And each side has genuine concerns and fears of who owns the customer relationship. The TV Operating System providers fear that HBO Max and Peacock’s large value proposition, on-demand and live content across general entertainment, movies, sports, and news, resides across multiple solar systems within the Smart TV galaxy. And could eventually evolve into its own video streaming platform, which reduces the value (or need) of the operating system due to the following potential risks by turning over the customer relationship (data):

Feature Parity with OS Providers: Content providers, by leveraging the intelligence on viewers, can improve their product discovery (e.g., content recommendation engine) and video experience to be on par with TV OS.

Viewers and Advertisers Shift to Content Providers: With content exceeding the OS providers’ value prop and product features on par, viewers can shift the majority of their viewing hours to the content providers, and advertisers follow suit—commoditizing the TV OS

Content Providers become TV OS: Content providers gain a dominant share in viewing hours and deep insights into viewers’ video needs, they could attempt to become a video operating system

In the reverse scenario, content providers have a heightened concern that TV operating system providers will reduce or commoditize their apps to eventually produce their own content, due to the following risks by owning the video experience and customer relationship:

Reduce Brand Value of Content Providers: With the video experience residing on the operating system platform and minimal branding opportunities, viewers develop a deep brand affinity for OS instead of the content providers

Viewers and Advertisers Shift to OS: If the lion’s share of viewing hours take place on the OS platform, advertisers would be inclined to spend on the OS versus with the content providers (e.g., Roku wants to sell 15% of ad inventory)

Content Parity with Content Providers: TV operating systems actively collecting data and drawing insights from viewers’ behavior enables them to create or license content that mirrors content providers

With both sides understanding the long-term implications, they have, for the moment, strategically decided to move forward without each other. HBO Max and Peacock believe that with their premium content, brand power, current distribution endpoints, they can achieve a sizeable user base—since launch, HBO Max has 4M subs and Peacock has 10M signups—to drive negotiation leverage as fans will demand that their services be on Smart TVs. But the operating system providers are “resting on their laurels” that these services will not be able to achieve user scale without having distribution on the most “lean back viewing” platform, hence agreeing to their terms. The dynamic of where the customer relationship lives not only exists with Smart TVs, but also with smartphones as well.

Smartphone: Customer Relationship Can’t Leave My Galaxy

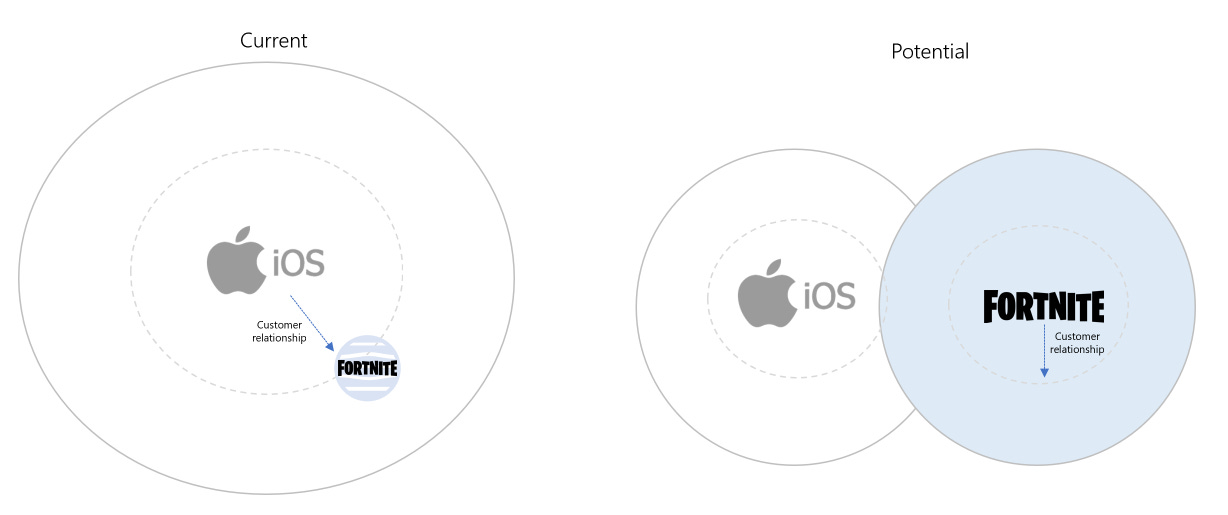

In the smartphone universe, Apple positioned a smartphone as a luxury good to not only attract over 900M active iPhone users but also the highest spenders—on average, iPhone users spend $250 per year. With the universe’s highest digital spenders, Apple’s iOS platform has attracted every human need category (solar system) and app (planet) to its galaxy. The gatekeeper to Apple’s galaxy is the App Store, a digital storefront that enables third-party companies to access their user base. But in return, the App Store takes a 15-30% platform (galaxy) fee. This business model has been very revenue generous as the App store drives $50B in gross revenue. But over 70% of the App Store’s revenue is being driven by gaming—the largest solar system in the iOS galaxy.

One of the largest planets in the gaming solar system is Fortnite, a free to play multiplayer video game set in a post-apocalyptic zombie world. Like most other games, Fortnite is shooter-led, but it takes a unique twist by adding a humorous and creative flair to “battling.” Players can personalize their characters by adding costumes, skins, and dances to bring joy during battle. Finding the intersection of achievement and creativity also informs Fortnite’s business model. Through Fortnite’s storefront, players can make microtransactions to purchase Battle Passes, for $9.50 per quarter, to get maps and game updates to better prepare for battle, and/ or purchase v-bucks, the platform’s digital currency, to buy new dances, costumes, and skins for their characters. By introducing a new business model and novel game concept that has captured the hearts of young adults and teens, Fortnite has an active install base of 350 million users and has generated $1.9 billion in revenue. But their revenue didn’t really skyrocket until Fortnite released its game into the highest spending galaxy of smartphone users, the iPhone.

“According to Sensor Tower estimates, Fortnite has reached 133.2 million installs and generated $1.2 billion spending on the iOS app store. In the last 30 days alone, 2.4 million installs and $43.4 million in revenue.”

That means that within a fiscal year, iOS players through Fortnite are driving at least 50-60% of Fortnite’s total revenue. And with the Apple tax of 30%, this equates to Fortnite sending 15%-20% of its gross revenue to Apple.

Fortnite, finding the access to galaxy fee too high, took a calculated risk by enabling payments within their app, so users can circumvent the App Store to purchase “v-bucks” for 30% less—no Apple Tax. Apple immediately disabled their app from the iOS platform, not only due to lost revenue, but fear of the following long-term implications by turning over the customer relationship:

Reduces Apple’s Utility Value: Having payments via the iOS, Apple’s Fortnite players perceive Apple as the utility value in helping them to unlock joy and achievement. But if payments are completely made via Fortnite, the perception of utility value shifts to Fortnite, reducing the need for the iOS (Hence why they have strict iOS payment rules)

Fortnite Players Become Device Agnostic: Fortnite has cross-platform play across smartphones, consoles, and PCs. If payments and storefronts are enabled within their app, it leaves very little room for devices to differentiate themselves for gameplay; hence, further commoditizing the value of Apple devices

Fortnite Evolves into OS: With payments enabled, Fortnite can evolve from just an entertainment metaverse, but also into the utility aspects of players’ lives, a place where players can order food, go on a date, pay bills and order clothes. Hence, shifting both players and developers to Fortnite’s platform

Payments are the last gravitational force keeping users tethered to Apple’s universe. By turning over payments, Apple fears that Fortnite will evolve from a planet in its own gaming solar system and, eventually, into its own universe. Apple has seen these long-term implications play out in China, as most users in China turn to WeChat to navigate their lifestyle needs, and not Apple.

In the era of data and intelligence, we will constantly see these collisions between galaxies and planets, as most applications and platforms want users to orbit around their products and services. Whether we need government intervention to settle the scores, or customers demanding to move across universes, space is at its best when astronomy affairs occur naturally, and not artificially (or forcefully) being tied to a universe.